")

Hugo Bilgram

Involuntary Idleness

An Exposition of the Cause of the Discrepancy Existing Between the Supply of, And the Demand For, Labor and its Products

PREFACE.

While engaged in the preparation of a treatise upon the subject of Social Rights and their relation to the distribution of wealth, the author had an opportunity to present some of the conclusions to which his studies have led at the meeting of the American Economic Association in Philadelphia, and on December 29, 1888, read a paper on “Involuntary Idleness.”

The Association having given but a brief abstract of the paper in the report of their proceedings, the author has been prevailed upon to publish the entire paper, and he is persuaded that its importance as a contribution to economic thought will be recognized by such students as regard the modern presentation of the science of Political Economy to be in many respects entirely unsatisfactory.

INTRODUCTION.

In order that the reader may more readily follow the line of argument developed in these pages, the following synopsis is presented.

The aim of the treatise is to search for the cause of the lack of employment, which is obviously due to the observed fact that the supply of commodities and services exceeds the demand, although reason dictates that supply and demand “in general should be precisely equal. The factor destroying this natural equation is looked for among the conditions that regulate the distribution of wealth, —i.e., its division into Rent, Interest, and Wages.

The arguments evolved by the discussion of the Rent question, which of late has excited much public interest, being unable to account for the apparent surfeit of all kinds of raw materials, the topic of rent is eliminated by assuming all local advantages to be equal.

At first an examination is made of the relation of capital to the productivity of labor, and that of interest on capital to the remuneration for labor, showing that high interest tends to reduce the productivity of, as well as the remuneration for, labor. Low wages being also concomitant with a scarcity of employment, it is inferred that a close relation exists between the economic cause of involuntary idleness and the law of interest.

Following this clue, the two separate meanings of the ambiguous word “Capital” are compared, showing that money, which can never be used in the act of production, cannot be capital when that term is used in its concrete sense; and since capital is capable of producing a profit only when the same is used productively, the fact that interest is paid for money-loans, when that which is loaned cannot be used productively, must be traced to an independent cause. The usual argument that with money actual capital can be purchased is rejected, because money and capital would not be interchangeable if their economic properties were not homogeneous. This compels the search for a property inherent in money that can account for the willingness of borrowers to pay interest on money-loans.

It is then shown that interest on money-loans is paid because money affords special advantages as a medium of exchange, and the value of this property of money is traced to its ultimate utility, or, in other words, to the increment of productivity which the last addendum to the volume of money affords by facilitating the division of labor.

Returning to the question of interest on actual capital,—i.e., the excess of “value produced over the cost of production,—the question as to what determines the value of a product leads to 1 the assertion that capital-profit must be due to an advantage which the producer possesses over the marginal producer. This is found to be due to the interest payable by the marginal producer on money-loans.

An ideal separation of the financial from the industrial world reveals a tendency of the industrial class to drift into bankruptcy by force of conditions over which they have no. control. Those who are at the verge of bankruptcy being the marginal producers, others who are free of debt will reap a profit corresponding to the interest payable by the marginal producers on debts equal to the value of the capital they employ; hence the rate of capital-profit will tend to become equal to the rate of interest payable on money-loans, and the power of money to command interest, instead of being the result, is in reality the cause of capital-profit.

The inability of the debtor class to meet their obligations increases the risk of business investments, and the accumulation of money in the hands of the financial class depriving the channels of commerce of the needed medium of exchange, a stagnation of business will ensue, which readily accounts for the accumulation of all kinds of products in the hands of the producers and for the consequent dearth of employment. The losses sustained by the lenders of money involve a separation of interest into two branches, risk-«premium and interest proper, and considering that the risk premiums equal the sum total of all relinquished debts, the law of interest is evolved by an analysis of the monetary circulation between the debtors and creditors.

This analysis leads to the inference that an expansion of the volume of money, by extending the issue of credit-money, will prevent business stagnation and involuntary idleness.

The objections usually urged against credit-money are considered and found untenable, the claim that interest naturally accrues to capital is disputed at each successive stand-point, and in the concluding remarks an explanation is given of the present excess of supply over the demand of commodities and services, confirming the conclusion that the correction of this abnormal state is contingent upon the financial measure suggested.

INVOLUNTARY IDLENESS.

In studying the past as well as the present drift of popular thought on political and economic questions, there is found not only a striking divergence of opinions, but on every hand doctrines are met that bear the unmistakable stamp of anomalous reasoning.

It is popular to attribute dull times and the consequent distress of the producers to an alleged overproduction of things, for the want of which people suffer. The immigration of those who are willing to add to our wealth by work and accept a small remuneration in return is considered detrimental to our well-being. The introduction of labor-saving machinery is contested by workmen in Spite of the saving of time and labor. International commerce is considered harmful to that country which receives more than it gives.

But in whatever form these self-contradictions appear, they evidently arise from the existence of an ever-present fear that there is not enough work to do, and that enforced idleness may inflict its miseries upon those who in the struggle for existence fail to secure their share of the work. Yet our experience, which indicates that the supply of services as well as of commodities does exceed the. effective demand for the same, is in direct conflict with rational thought. Whatever is offered in the market for sale is ostensibly offered with the expectation of obtaining something else in return, either directly or through the medium of exchange. Each supply of a commodity, each offer of a service, implies a demand for some other valuable thing or service. The more commodities one man makes and offers for sale or exchange, the greater, it appears, should be the demand for other commodities. But while there is every reason to assume that the total supply of commodities and services in general should always equal the total demand, we notice in reality the absence of such an equation, we know that labor can become a drug in the market. The competition of those unemployed, who are in search of work, produce the long-recognized tendency of wages to a minimum of subsistence and give plausible pretext to the doctrine of socialism. Tariff legislation, as well as that regulating immigration, the time of labor, etc., and other laws designed to regulate competition, testify in unmistakable terms that the fear of competition, the dread of involuntary idleness, is not an empty phantom, but a stern reality. Most painful is the effect of enforced idleness when it manifests itself in industrial depressions, those social calamities which the science of economics has so far failed to explain satisfactorily.

The standard works on Political Economy, such as Ricardo’s, Mill’s, etc., fail to reveal the cause of the manifest discrepancy between what obviously should be and what really is. In fact, the method of those writers in dealing with definitions and propositions is in marked contrast with that adopted in the exact sciences. The use of ambiguous terms has led to unwarranted and incorrect applications of otherwise correct doctrines. Well-established propositions being sometimes admitted and at other times unceremoniously ignored, contradictory statements are not infrequently found, which impair the reliability of the conclusions of those writers. But although they have in a measure failed to dispel the confusion of popular views, there is no reason why social phenomena should be more difficult to analyze than those of a physical or chemical nature. It should therefore be possible to find, by logical deduction, the fundamental cause of involuntary idleness, or the factor which destroys the natural equation between the supply of, and the demand for, commodities. And this can be found only among the conditions that regulate the distribution of wealth and determine its division into Rent, Interest, and Wages.

The thorough ventilation which the relation of Rent to the Social Problem has received through the works of Ricardo and his followers, especially Henry George, while showing that a lowering of the margin of cultivation can account for a lowering of wages by a reduction of the productivity of labor, has brought forth no clear explanation for the excess of the supply of commodities and services. As long as there exists any uncultivated land capable of affording a living to its cultivator, the law of rent cannot account for enforced idleness. The study of the economic causes which produce, as well as the laws which regulate, capital-profit, or interest proper, have in the interim been comparatively neglected. It is therefore not inappropriate to give more thought to the relation which interest bears to wages. A rational analysis requiring the exclusion of all matter foreign to this relation, the question of rent should be eliminated by assuming for the time being that all natural and local advantages were equal.

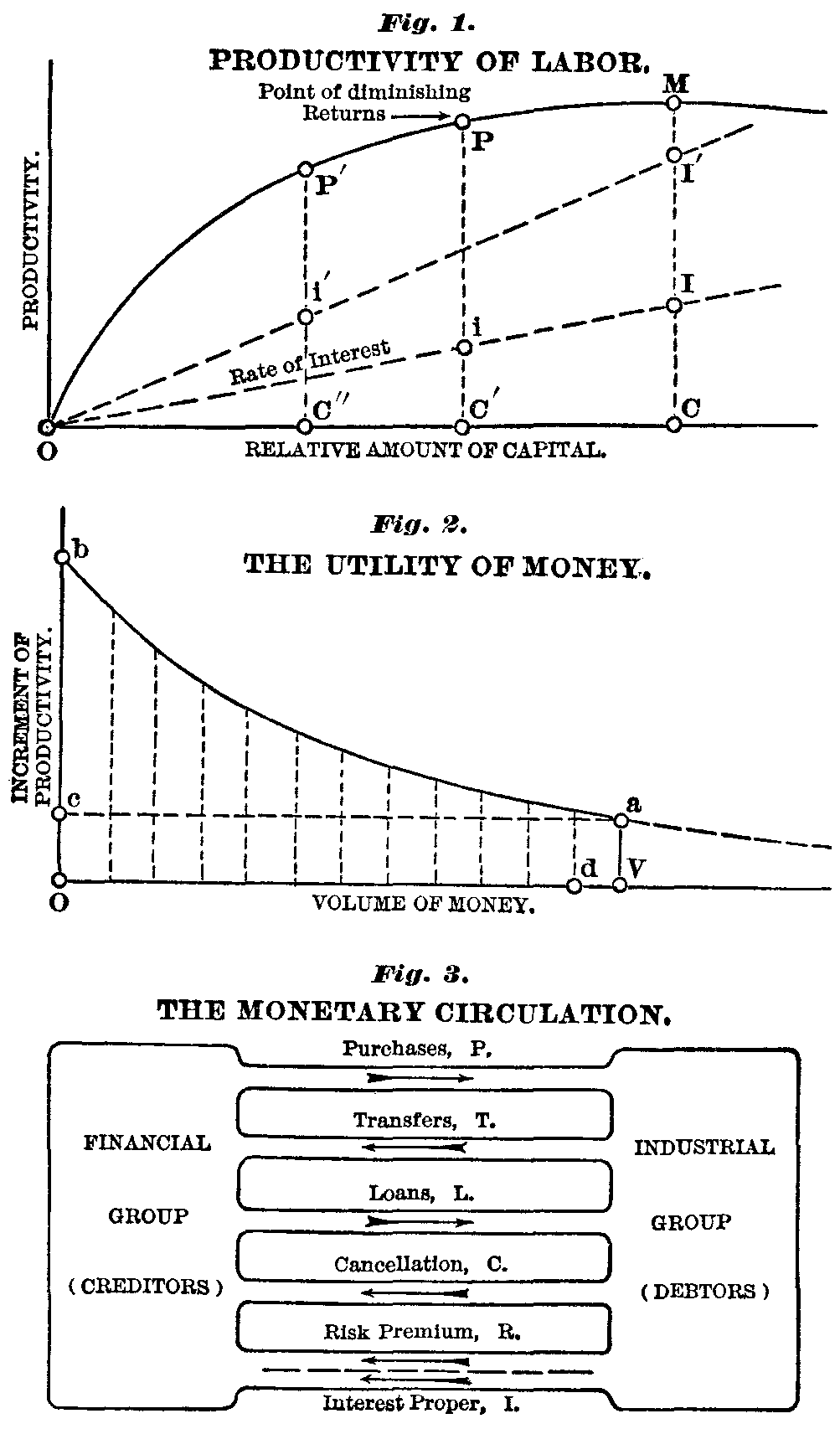

While nature furnishes the substance of all wealth, labor and capital are the factors that give this substance value. The productivity of labor depends, however, in a great measure upon the amount of capital employed. If some one, desiring to produce certain commodities, could have the assistance of, say, one hundred men, the productivity of their labor would be very low if no auxiliary capital were applied. The use of crude tools would decidedly increase the efficiency of their efforts, and if more capital in the form of improved auxiliaries were added, the productivity would be still greater. There is, however, a limit to this increase of the productivity of a given number of men by the addition of capital, because capital, when used productively, will deteriorate, and a portion of the labor must be diverted for the purpose of restoring this loss. As the amount of labor so diverted grows with the increase of capital, it is evident that the productive power of labor will not keep pace with the addition of capital, and that a point can be reached beyond which a further increase of capital will have an adverse effect and actually reduce the net productivity of those one hundred men. The variation of their productivity due to an increase of capital can be represented by a curve of the character shown in Fig. 1. (See plate at end of volume.)

For reasons just stated this curve will decline after passing the apex M, which represents the highest possible productivity of the stated amount of labor. The contingency of a future progress in the methods of production, which would affect the course of the curve, is of course not considered.

Although the productivity is at a maximum when an amount of capital equal to OC is employed, the employer will not find it to his advantage to apply this amount, because of the interest-bearing power of capital. Letting the distance CI represent the interest due to the capital OC, this amount must be deducted from the value produced, leaving the value IM, from which the employer must defray the cost of labor, the remainder being his wages for the management of the business. By using an amount of capital equal to OC, the interest would have amounted to Ci, and the return to labor and management, iP, would exceed the quantity IM. The most advantageous proportion of capital can be located in the diagram by finding that point, P, at which the curve is parallel to the interest-line OI, and it is the tact of successful business-men to closely approach this point in their management. The point P bears the same relation to capital as the point of diminishing returns does to land.

If the rate of interest payable on the capital OC had been CI’, the high rate would have caused the employer to apply capital more sparingly, and our diagram would in fact indicate that the productivity C”P’, due to the capital OC”, will give the best result. On the other hand, if the producers could have abundant capital without interest, labor would be employed most advantageously at its natural maximum of productivity.

The diagram clearly illustrates the separation of the value produced by labor and capital into interest and wages, the remuneration of the manager being considered wages. But while so far we can see no indication as to what determines the rate of interest, it will be perceived that as interest rises wages become less, for the productivity of labor will be reduced by the more cautious use of capital, and, besides, a greater proportion of that which has been produced will go to capital as interest. The remuneration of all labor is represented by i’P’ when interest is high, by iP when interest is low, and it would be equal to CM if capital could be obtained without interest. This proposition is true only for a state of persistency, when no secondary factors intervene, and not for transitory periods of industrial activity. If from any cause persistency is disturbed, the disturbing factor may for a time change this relation between wages and interest, and make wages and interest rise or fall simultaneously. We shall see that the cause of involuntary idleness is just such a factor.

In comparing the proposition that under otherwise equal conditions a high rate of interest tends to reduce wages with the indisputable fact that when many men are without employment wages are low, a strong suspicion is raised that an intimate relation may exist between the economic cause of high interest and that of involuntary idleness; for there is no phenomenon which can have two independent explanations. We are therefore justified in pursuing the investigation by searching for the law that determines the rate of interest.

This inquiry must be directed, not so much to the cause of the increase of productivity attainable by the use of capital over that of productive efforts made without the use of auxiliaries, but to the economic causes that assign to the owner of capital a portion of. that which is produced by the co-operation of capital and labor.

In order to discriminate intelligently between the conflicting definitions of the term “Capital,” as given by the authorities, we should first understand why a distinction is made between wealth which is, and wealth which is not, capital. Experience shows that wealth under certain conditions is capable of bringing a revenue to its owner, and this power fully justifies a classification being made. There being no other economic difference of importance, it must be accepted as the real motive of this differentiation of wealth. Adam Smith defines the term by this power, and is followed by others, notably Macleod. There is, however, a strong tendency among modern writers to depart from this natural definition with a view of indicating the source of this power. According to John Stuart Mill capital is the accumulated produce of labor requisite for further production. The term “Capital,” therefore, covers two totally distinct concepts, which are frequently confounded to the detriment of correct reasoning. Capital, in its abstract sense,—comprising all wealth capable of bringing a revenue, —admits the conception of a “conversion of capital” or of “floating capital,” etc., not referring to any particular thing, but to wealth in general when it has a certain economic relation to its owner, while in its concrete sense,— meaning certain things produced by labor, and used for certain purposes,— its conversion is inconceivable. Yet the adherents of the concrete definition adopt these phrases without even suspecting the logical error. Moreover, the concrete definition, if not further qualified, lacks the feature of exactness, in not stating whether wealth is capital whenever it is capable of being used productively, or only as long as it is in productive use. There is, however, no room for dissent. The mere ability of things to be used in production, if they are not so employed, cannot account for the revenue-returning feature, which being the distinguishing attribute of capital, it is plain that not the potentiality of wealth, but its actual use alone can turn wealth into capital. Nor does this definition cover objects which are being consumed unproductively, such as private residences rented to tenants, etc. A hired equipage is aiding further production no more than a private carriage, yet in one case it is capital, in the other it is not.

Another inconsistency is shown by the exponents of the concrete definition when they include money in the category of capital, while in reality money as such neither is nor can be used in the act of production, and therefore never can be a requisite for further production. This is admitted either directly or by implication by most economists. Newcomb asserts that “the money serves the banker no useful purpose until he passes it to some one else, perhaps a customer. Every one into whose hands it falls must be paying or losing interest on it while he keeps it, and he cannot gain the interest until he purchases an ownership in some form of actual capital.” This is clearly an admission that interest must be paid or will be lost on money wherever it may be, or to whatever use it may be put; for even if actual capital is purchased, the loss of interest must be borne by the one to whom the money is transferred. Money being thus admitted to be unproductive, it cannot be considered capital if the definition of Mill is adopted, and any preposition relating to capital and demonstrated under this definition cannot be consistently applied to money. It is therefore important to pay special attention to the interest-bearing power of money, the real source of which is not generally recognized.

In the following discussion the term capital will be used in its concrete sense.

The income derived from wealth, whatever be its form, can be acquired by its owner in two ways. fie may use the wealth productively, or, by loaning it to others, receive a premium for its use. In the one case the income accrues as profit, consisting of the excess of value obtained over and above the market value of the labor applied and other expenses incurred; in the other case it appears as interest proper, which is equal to the gross interest minus the rate of risk and deterioration. But since he who borrows capital is willing to give interest because the use of capital will give him a material advantage, it follows that profits derived from loans must be considered mere transfers of the value of this advantage.

Applying this preposition to the interest-bearing power of money, we are confronted with the fact that money cannot be utilized as a requisite of production, and is therefore incapable of bringing an excess of value in this respect. Consequently we are. obliged to look elsewhere for any benefit which may be derived from its use. It is true, we are told that with money actual capital can be purchased from which profit may be obtained. John Stuart Mill says, “Money, which is so commonly understood as the synonyme of wealth, is more especially the term in use to denote it when it is the subject of borrowing. When one person lends to another, as well as when he pays wages or rent to another, what he transfers is not the mere money, but a right to a certain value of the produce of the country to be selected at pleasure, the lender having first bought this right by giving for it a portion of his capital. What he really lends is so much capital; the money is the mere instrument of transfer.”

In this proposition it is assumed that money is not necessarily wealth, but a right to a certain amount of wealth, and that the lender of money has received his money by giving a portion of his capital for that which is merely an evidence of such surrender of capital coupled with the right to demand an equivalent at pleasure. This right is what is transferred to the borrower, who can use the capital so obtainable, and for this use pays interest. To an unprejudiced mind several pertinent questions will naturally arise. If society has obtained capital for which it has given merely a right to demand an equivalent, why does not society pay for the use of that capital, indemnifying the holder of money for his abstinence, until that right to demand has been redeemed? If Mill’s reasoning is correct, somebody must have the lender’s capital even before he lends the money to others, and justice would require that the interest gained by its use should be paid to the holder of money by the user of that capital. Moreover, why is it that the borrower of money must pay interest for the mere right to select capital before the selection is made? During the interval between the borrowing of money and the selection of capital society has the use of that capital, and society rather than the borrower of money should in equity bear the burden of interest. Furthermore, why should the borrower of money pay the interest to the lender who has given his actual capital to somebody else, instead of paying it to him who renders the service of giving actual capital for a mere evidence of surrender and right to demand an equivalent?

If capital has reproductive powers while money has not, it is not reasonable to assume that anybody would willingly exchange actual, profit-bearing capital for money, on which interest will be lost, if money should not afford some other equivalent advantage, and notwithstanding the assertions of authorities we must look for a property inherent in money which alone can account for the willingness of borrowers to pay interest to the lender of money.

As regards concrete capital,—i.e., products of labor applied to further production, there can be no doubt that profits can originate only while it is used in combination with labor. Capital profits will therefore invariably appear in conjunction with wages, in the manner shown in the diagram Fig. 1. (See plate at end of volume.) The term production must here of course be understood in its broad sense. Goods exposed for sale, aggregated with others of a similar nature, though apparently out of use, are really in the stage of commercial production, the process of distribution requiring them to remain, for a time, in a seemingly inert state. Industrial capital may also be temporarily out of use without ceasing to be capital as this term is commonly accepted. Machines are usually idle not only fourteen hours each day but also one day of each week.

But the requisites of production may be out of use for quite other reasons. To be productively employed they must be aggregated in certain combinations. A power-loom, for instance, can be in industrial use only when located in a suitable building, when connected by shafting and belting with a motor, when supplied with yarns to be woven into a fabric, and when attended by a mechanic skilled in the art of weaving. Each of the numerous branches into which production is divided requires a peculiar combination of raw materials, auxiliaries, and human skill. Any product passing through the various processes in the course of its economic maturation becomes alternately a raw and a finished product, the finished product of one group of producers being the raw material of those that follow.

Regarding a single group, the wealth in course of generation, after passing through the process peculiar to that group, becomes a finished product, ceasing to be a requisite of production to this group, and is to all intents and purposes inert wealth or idle capital. In this form it is virtually no-interest capital, and has the same function in the theory of capital-interest that no-rent land has in the theory of rent. It can be vivified or converted into live capital only if transferred to another group, in which it will find that combination of capital and skilled labor congenial to its further maturation.

But in the present quasi-individualistic state of society such transfers are always contingent upon the return of equivalents. These exchanges would be beset by serious obstacles, practically forbidding a division of labor, if the special instrument of exchange, money, were unknown, which though not a means of production, is a very essential factor in our industrial system. Without it those transfers which convert inert wealth into active capital and render possible a division of labor would be almost impossible.

This will explain why an owner of actual capital is willing to exchange it for money on which he will lose interest while possessing it. The capital he is willing to give for money has manifestly arrived at that stage of production when it is to him a finished product and requires to be transferred to other producers to become live capital, while he in turn requires capital which is inert to others but capable of further productive manipulation by him. To accomplish these transfers, money is the indispensable instrument. One of the most important phases of this function is the paying of wages,—i.e., the distribution, among the producers, of the increment of value which accrues to all products as they pass through the various stages of production.

This analysis leads to the inference that interest on money-loans is paid because money affords special advantages as a medium of exchange, and the fact that most money transactions of to-day are made by means of paper evidences without transfer of actual wealth confirms this conclusion. A loan of bank-notes on security is admittedly an exchange of two rights of action,—one, the security, having a precarious, the other, the money, having an ever-ready value. The right of action which the banker accepts as security can be exchanged for other things, or realized, only on certain conditions, while that which he gives is readily accepted everywhere at its face value. This universal acceptability gives to money its special advantage, and being the only important difference between the two rights of action, the payment of interest can be traced to no other feature of money.

We can now proceed to investigate the value of this advantage and its relation to the rate of interest. In a community in which, for the want of money, barter is the sole method of exchange, an extensive division of labor with its attending advantages would be impossible. A limited supply of money can only partially improve this condition, but it would naturally flow into those channels in which the resulting advantages are greatest. A second equal supply, while likewise augmenting productivity by permitting a further division of labor, would not increase it in the same measure, the channels of the first order being filled. A third equal supply would further increase productivity, but in a still less degree. The general advantage afforded by money can therefore be represented by a curve, as shown in Fig. 2 (see plate at end of volume), the ordinates representing the increase of annual productivity contingent upon the corresponding increment of the volume of money represented by the abscissae, each new addition corresponding with a diminishing advantage.

Now, although the successive additions to the volume of money produce different effects as far as the general good is concerned, the law of supply and demand will tend to accord to all money in the same market an equal rate of interest, and it can be demonstrated that this rate will adjust itself to the ultimate utility of money, namely, the annual increase of productivity, Va, afforded by the last addendum, dV, of the total volume of money, OV. For if the owner of this last quantity of money expected a higher rate, he would find all channels capable of rendering such a rate fully supplied, and must therefore be content with the advantage of the best channel yet open. He being the lowest bidder, this obviously determines the market rate of interest, as indicated by the horizontal line ca.

The diagram now plainly shows the separation of the total benefit derived from the division of labor attainable by the use of the volume of money OV, and represented by the area OcbaV, into two parts; the oblong OcaV incloses that part which the law of supply and demand will apportion to money as interest, while the remainder, the area cba, will accrue to capital and labor. The diagram also appears to indicate that the rate of interest on money-loans, other things being equal, will depend on the volume of money in circulation, whenever the law of supply and demand is free to operate.

The inquiry as to the economic cause of the profit which accrues to wealth used productively can now be continued. Such profit can arise only if the value created by the combination of capital and labor exceeds the cost of labor; that is, if the value produced exceeds the cost of production, this cost including the value of the labor of the employer. Here the question naturally arises, What determines the market value of that which is produced, and when and why does it exceed the cost of production? In answer we must refer to the law of supply and demand, the effect of which is thus definitely expressed by Ricardo: “The exchangeable value of all commodities, whether they be manufactured, or the produce of the mine, or the produce of land, is always regulated not by the less quantity of labor that will suffice for their production under circumstances highly favorable and exclusively enjoyed by those who have peculiar facilities of production, but by the greater quantity of labor necessarily bestowed on their production by those who have no such facilities; by those who continue to produce them under the most unfavorable circumstances; meaning, by the most unfavorable circumstances, the most unfavorable under which the quantity of produce required renders it necessary to carry on the production.”

Ricardo has evidently in mind those things which are produced under different degrees of difficulty, the quantity produced under the most favorable conditions being inadequate to supply the demand. The total demand determining the margin of the least favorable point at which production will be continued, Ricardo’s law of value can be briefly stated as follows: The natural value of those things that are being reproduced is always- equal to their cost of production at the margin of production. Conceding this proposition, it follows that every profit must be traceable to an advantage which its recipient possesses over the marginal producer, and, moreover, that no persistent profit can possibly arise unless there be a difference in the opportunities of production. In continuing our inquiry we must look for such a difference.

It would be an error to bring into consideration the difference of abilities of employers. The so-called profits of the enterprising business manager are, as a rule, a remuneration for valuable services rendered, and properly belong to the category of wages. Our object is to find the economic cause which apportions a share of the produce to capital independent of its owner’s ability or assistance as a worker or manager. There is but one class of variable producer’s expenses having the character of a disadvantage that has any direct connection with our subject. Those who do not own all the capital they are using must pay interest on their indebtedness, which increases their actual outlay over that of business-men free of debt. The question is now, should this outlay be considered an unavoidable addition of the cost at the margin. If it were paid because of the profit-bringing power of the borrowed capital, then the solution of the problem would be as remote as ever. But if there be some other economic factor compelling this outlay, its examination may reveal that which we are in search of.

Business debts are, as a rule, contracted not by borrowing actual capital, but by borrowing money, and, as we have seen that money bears. interest solely on account of its attribute as a medium of exchange, and have taken issue with the prevailing impression that the borrowing of money is a borrowing of capital, we must search for the reason why business- men so largely depend upon loans to procure the medium of exchange.

Were it possible to separate by a sharp line the financial from the industrial world, these who issue and those who loan money from those who produce wealth, the flow of money between these two groups would present a very striking feature. The industrial group could obtain the medium of exchange requisite to carry on commerce in but two ways; by selling the products of their labor to the financial group, and by borrowing money from them. By the first measure the transfer of money from one to the other group is absolute, by the second it is conditional upon a return of the principal with the addition of interest. Loans, as a rule, imply a return of a greater sum of money than was loaned, and the only persistent source from which this excess can be drawn is obviously the first mentioned way of obtaining money. These receipts from sales are, however, not so much regulated by the productivity of the debtors as by the willingness of the creditors to buy that which the debtors offer for sale. And since money loaned to others is a source of income, it is quite natural that the creditors will not only reinvest the principal, but will reserve a part of that which they receive as interest for additional investments. Hence only a portion of the money Which the debtor class pays as interest to the creditors will return to them by the regular channels of commerce, and the receipts of money, by the industrial group, from sales to the financial group being for this reason less than the amount of interest paid, the primary effect will be a reduction of the money circulating among the producers. Some of the channels of commerce, that were previously filled with the requisite medium of exchange, having been thus depleted, the members of the industrial group will be induced to borrow not only that money which had been returned as principal, but also that which the financiers had reserved for additional investments. This measure will increase both the indebtedness and the obligation to pay interest, augmenting the discrepancy between the amount of money received through sales and that expended to pay interest, the growth of indebtedness assuming more or less the nature of a geometrical progression. This cannot continue forever. It not only becomes a physical impossibility for the debtors, as a class, to ever satisfy their creditors, but they are irresistibly driven, by the fatality of these conditions, into bankruptcy.

These conditions do in reality exist in our present social system. Even though the distinction between the financiers and the producers is not as sharp as outlined in the above analysis, the premises are, notwithstanding, amply justified. By virtue of “our financial, “laws, which forbid the issuer of bank-notes to use them for industrial” purposes, this money can be brought into circulation only by the creation of a debtor class, which is necessarily recruited from the industrial group. It is true, the pressure, which we have seen will inevitably result, will not fall with equal severity upon all men engaged in production. Many will keep out of debt, while others will succeed in freeing themselves from that burden. But since interest must be paid in money, and the debtors as a class cannot indefinitely pay more than the amount they realize from sales to the creditors,—these sales being inadequate to restore to the debtors the means of paying the interest, owing to the fact that the creditors apply a portion of their income to additional investments,— the inability to pay must result in the failure of the less successful of the producers despite their industry and intelligence, not for the lack of business capacity, but because their competitors are abler than they. They will continue to produce until their debts exceed the value of their capital, when, being driven beyond the margin of successful competition, they must succumb to the inevitable. We here recognize a condition which inexorably forces upon the producers an ever-increasing indebtedness and obligation to pay interest, precipitating one after another into insolvency. Those who are at the verge of bankruptcy, being indebted to an amount equal to the value of the capital they employ, are obviously the marginal producers, and as the natural value of the products will equal the cost of production to them, all producers whose capital is unencumbered will obtain a profit equal to the interest payable on borrowed money by those marginal producers.

This course of reasoning would indicate that, quite contrary to the generally received doctrine, the power of money to command an interest is not the result, but the cause of capital-profit.

This is, however, not the only important conclusion to which this analysis leads. The logical results of the conditions depicted agree so fully with all the phenomena common to business depressions, that no more complete verification of the theory can be desired. As the indebtedness of the producers grows with an ever-increasing rapidity, they cannot indefinitely continue to contract new loans. Money will accumulate in the hands of the financial class instead of circulating in the channels of commerce. The inability of the producers to meet their obligations will become general, investments will become hazardous, and a portion of the interest must be devoted to cover the occasional losses of the creditors, the remainder alone being a real source of income. Interest will thereby be separated into two parts, the risk premium, or insurance to balance the deficiency of the principal returned on loans, and the interest proper. The law of supply and demand no longer dominates in fixing the rate of interest. Its operation is impeded by the inability of the debtor class to return more money than they receive. The determination of the rate of interest proper must therefore be relegated to another law, born of the same conditions that produce the deplorable results so characteristic of our present industrial development. The constant drain upon the money in circulation paralyzes commerce and obstructs the division of labor. Products in various stages of completion accumulate in the hands of the producers who cannot transfer them for further productive manipulation. The means of production are lying idle and workmen skilled in special trades cannot find employment; The financiers, in whose hands the money accumulates, are anxious to loan it at low interest on good security, but the general stagnation of business renders all investments insecure or unprofitable. Thus we find a ready explanation of the phenomena of business depression, and can discard such insufficient and illogical though popular explanations as a general loss of mutual confidence, speculation, accidental coincidence of unsuccessful enterprises, excessive railroad construction, over-production, keen competition, strikes, etc. All these alleged causes are in reality merely symptoms of the same social disorder.

For the analytical deduction of the Law of Interest see Appendix.

When by purely deductive reasoning we arrive at conclusions so completely corresponding with experience, it is reasonable to accept their promptings as to the proper method of avoiding industrial stagnation, which our investigation has shown to be engendered by an insufficient supply of money. We are naturally led to ask, What limits the volume of money? Before the development of the modern banking system, when the precious metals were the almost exclusive money-medium, the volume of money could not exceed the amount of those metals. But since the use of credit as a medium of exchange has been established, the extent to which the money-volume can be increased is almost unbounded, encompassing the entire credit of the business world, which is undoubtedly the natural limit. Our financial laws, however, by strictly circumscribing the emission of credit-money, impose an artificial barrier, the removal of which would put an end to the involuntary idleness which the onerous toll for the use of money occasions. But since an issue of money, limited only by the effective credit, would be a radical departure from our present system, it is proper to examine the principal objections urged against it,—the ease with which it can be abused, and its effect upon the purchasing power of money.

The first of these objections is not justified, since the abolition of an arbitrary limitation need not involve the withdrawal of the ordinary safeguards that restrain the unscrupulous. To prevent fraud and imposition the government has been invested with the power to furnish money, guaranteeing its value, and controlling its issue. But restrictions are made that are not in harmony with this reason for confining the regulation of credit money to the government, and they are primarily responsible for the scarcity of money and its consequences. The unlimited issue, by the government, of credit money to those furnishing proper. security, precisely as it now loans notes to the national banks, with this difference, that not only national bonds, but any adequate security be acceptable, while removing the arbitrary limit, would in no wise facilitate abuse. The risk involved in accepting securities other than bonds could be met by a charge of interest sufficient to cover these losses, the rate of such risk being readily ascertained. In the absence of an arbitrary limit the volume of money would be free to expand in proportion to the effective demand, and the rate of interest being reduced to the rate of risk only, interest proper for the use of money would cease.

To be sure, capital as well as money when loaned will continue to bring a return, but the law of supply and demand operating without artificial restriction, the pay for the loan of capital will naturally adjust itself to the economic value of its use,—i.e., the rate of risk and the deterioration of the capital loaned. Only the apparent power of capital to more than reproduce itself, the ability to bring a persistent revenue, will terminate.

The removal of the artificial impediment to the free conversion of sound credit into money would have a. vital bearing upon the Rent question which is now exciting considerable interest in economic circles. A reduction of the current rate of interest is known to have the effect of raising land values, and if the rate of interest proper were reduced to zero, land values would obviously rise until the taxes, if assessed pro rata on the value of real estate, will practically absorb all of the economic rent. The nationalization of the economic advantages of natural and local opportunities would therefore result without any further legislation on the subject.

The second objection, founded upon the assertion that the purchasing power of money is always inversely proportional to the total volume, other things being equal, is widely accepted as conclusive. Were it true that an increase of the volume of money would be balanced by a reduction of the value of each dollar, the capacity of the total amount of money to perform its function would remain unchanged, and under such circumstances the measure suggested would obviously be futile.

This theory of the value of money, though disputed by some economists, is vigorously defended by most English and American writers. Ricardo asserts: “That commodities would rise or fall in price, in proportion to the increase or diminution of money, I assume as a fact which is incontrovertible.” Yet the strongest arguments that can be adduced against this position are found in this writer’s works. He unqualifiedly declares that the value of any article capable of reproduction is equal to the highest cost at which its production is continued, the cost at the margin of production. It is therefore remarkable that in the quotation referred to this law of value, which has been so properly applied in the theory of rent, has been totally ignored, especially since he admits that, “While the state coins money, and charges no seignorage, money will be of the same value as any other piece of the same metal of equal weight and fineness; but if the state charges a seignorage for coinage, the coined piece of money will generally exceed the value of the uncoined piece of metal by the whole seignorage charged.” Here it is plainly acknowledged that the value of money equals its cost of production. Now, if this proposition is true, the value of money can rise or fall, or prices in general can fall or rise, only if the cost of producing money is changed, and the volume of money already in circulation cannot influence this value. If, on the other hand, the quantity of money in circulation determines the value of money, this value, in consequence, would be independent of the cost of production. Obviously one of the two Ricardian propositions must be wrong.

John Stuart Mill follows Ricardo very closely. In two consecutive chapters he expounds both propositions, and attempts to harmonize them by referring to a particular illustration in which the contradiction does not present itself plainly. Other inconsistencies are disposed of in an equally remarkable manner. After showing that money is merely a contrivance for facilitating exchanges, the mode of exchanging things for one another consisting in first exchanging a thing for money and then exchanging the money for something else, he asserts that “The value or purchasing power of money depends, in the first instance, on demand and supply.... The supply of money ... is all the money in circulation at the time.... As the whole of the goods in the market compose the demand for money, so the whole of the money constitutes the demand for goods. The money and the goods are seeking each other for the purpose of being exchanged. It is indifferent whether, in characterizing the phenomena, we speak of the demand and supply of goods, or the supply and the demand of money. They are equivalent expressions.”

This proposition leads to a very remarkable inference. Conceding that the seller of things wants money only for getting other things, then the demand for money is virtually a demand for those other things; and since the supply of goods and the demand for money are “equivalent expressions,” and the denial for money really means a demand for goods, it must logically follow that the value of all money must equal the value of all goods offered for sale. This conclusion is obviously at variance with facts. It is true, in the same chapter this very inference is repudiated, — but this involves a qualification which reflects disastrously upon the original preposition. The logic of a writer can fairly be questioned who propounds a doctrine, repudiates one of its corollaries, and then finds fault with others for refusing to accept this preposition as incontrovertible.

Professor Newcomb attempts to show by the equation existing between the industrial or societary and the monetary flow that prices in general must rise or fall as the volume of money is increased or reduced, but the fact appears to have escaped his attention that a restriction of the money-volume necessarily reacts upon the corresponding industrial flow, which renders untenable his conclusion based on a constant industrial flow. It is the amount of societary circulation and eventually the rapidity of circulation, and not the value of the dollar, that will respond to a change of the volume of money. His. equation, properly interpreted, proves conclusively that the limitation of the volume of money, in being attended by a restriction of the monetary flow, must react unfavorably upon the industrial flow and consequently produce business stagnation.

The opinion that the value of money bears an inverse ratio to its volume originates from a misconception of the nature of credit-money, resting on the absurd belief that value can be created or changed by the flat of the government. Even though the followers of Ricardo contest this view, they inadvertently commit themselves to it in their doctrine of the value of the so-called inconvertible notes. They aver that such notes, when brought into circulation while coin is yet in use, in driving the coin out of circulation assume a value equal to that of the precious metals thus displaced. This would obviously imply that the issue of such notes does increase the wealth of a country.

There is but one rational theory of credit-money. The note is merely an evidence that the bearer has a right of action against the issuer,—in other words, a qualified right of ownership to wealth held by the issuer of the note,—and its current value equals the amount of wealth or services obtainable, or supposed to be obtainable, for this evidence from the issuer. The value must of course be specified by reference to a value unit,—usually a definite weight of silver or gold,—in which the notes must be conditionally redeemable, but not necessarily on demand, and a depreciation from this nominal value can occur only if the issuer fails to fulfil his promise and the holders of the notes are unable to compel such fulfilment. As regards their value, banknotes as well as the so-called inconvertible notes are essentially analogous to mortgages, promissory notes, and other evidences of indebtedness, and any attempt to apply the volume doctrine to the value of the latter would properly be condemned as a fallacy. Why, then, should it be true if applied to credit-money? If a bank-note is a receipt, showing that the holder has surrendered some value, it must also specify reciprocally as to who has received this value, and will return it when the note is retired. The members of society severally can surely not be held responsible for what one person has given to another; they will therefore not accept a note unless they have the assurance that the issuer, who is the first recipient of value for the mere paper evidence, will ultimately redeem the note by giving the specified value for it. The so-called inconvertible notes contain the premise of redemption by implication only; and whenever the government accepts them in payment of taxes—that is, in exchange for services rendered—this promise is fulfilled. But not being definitely expressed, governments have often taken advantage of this looseness of contract, and have violated what should have been a sacred obligation. Even now the opinion prevails that the excess of the nominal over the intrinsic value of subsidiary coin is a legitimate “Profit” to the government, contrary to the dictates of honesty, which demand that this excess should be viewed as a temporary surrender of value by the bearer of the coin, to be returned when the coin is retired. Unfortunately, it is not generally recognized that in money three factors are essential: first, the token; second, wealth in the control of the issuer and obtainable, or supposed to be obtainable, in some form by the holder of the token; and, third, the general agreement which makes the token universally acceptable. In making the token of gold weighing 25.8 grains per dollar, any further guarantee is superfluous, but if only a portion or none of the value accompanies the token, the deficiency is supplemented by a right of action or its equivalent against the issuer. For this reason depreciation cannot take place unless the holder of the token is unable to obtain the promised value from the issuer. Should the government furnish money-tokens to all those who give proper security in the form of rights of action against their possessions, the property so involved would be the basis of the value of these notes, the government holding the rights of action to insure the ultimate redemption of the notes.

It is frequently urged that the French assignats are an example of the evil effects of an expansion of credit-money, while in reality their depreciation must be attributed to a virtual absence of any Specific right conferred by their possession. While their value was alleged to be founded upon land, neither the amount of land nor its value was in any way defined upon the notes, and a statement of value or exchangeability having thus been omitted, their value was purely imaginary, and they could circulate only as long as there was a hope of an ultimate redemption. The United States greenbacks depreciated for no other reason than a partial repudiation, consisting in the refusal of the issuer to accept them for all debts at face value,—i.e., 25.8 grains of gold per dollar. Manifestly, the idea that the volume of money has any effect whatever upon the purchasing power of the dollar—except in the measure in which a change of the volume of coin may affect the demand for, and hence the commodity value of, gold—is a gigantic delusion, warranted neither by theory nor by facts, and the second objection to an extensive issue of credit-money falls to the ground. There remains no reason to fear any evil effects of an expansion of the money-volume while it remains within the bounds of substantial credit.

But few words are needed to show how insufficient are the current theories that seek to account for the reproductive power of capital. There are really but two doctrines in vogue, the one ascribing interest to the increased efficiency of labor when supplemented by proper tools, the other claiming that men will not forego the present use of wealth without compensation for their temporary abstinence, and that this payment is necessary to induce people to make and save wealth to be used as capital.

An illustration will enable us to examine the correctness of the utility doctrine.

Since a tailor can do more work by using a sewing-machine than he can by hand, rather than do without the ma- chine which he may be unable to purchase he will gladly give a portion of the increased production for the hire of such a machine. This is altogether true, but what does it prove? It certainly proves nothing in regard to capital-profit. The same argument might be offered to demonstrate that all drinking-water must have a price because any man famishing from thirst would willingly pay a high price for a drink. Returning to our illustration, let it be assumed at first that only one man can make sewing-machines, he being the patentee. The tailors will no doubt offer as, a hire a part of their extra earnings, and the supply of machines being inadequate, those wanting machines, in competing against each other, will offer almost the entire advantage gained by the use of the machines. We must of course take into consideration that the aversion of tradesmen to change their wonted method of working and other elements reduce the estimated advantages below the actual increase of production. With this qualification it can be said that there exists an economic tendency to give to the sole maker of the machines approximately the entire advantage gained by the use of the machines.

But after the patent expires and others can make sewing-machines, their supply will rapidly increase because they will be a profitable investment. Then the owners of the machines will compete, and the rate of hire will fall, involving a cheapening of the produce of the sewing-machine, the consumers of which will reap that part of the benefit resulting from the invention which ceases to be returned to the owners of the machines. The question is now as to how far competition will tend to depress the hire. Why is it that the law of supply and demand assigns only a portion of the benefit of the invention, after it has become public property, to the consumer of that which has been produced on the machine? Why is it that a portion of that which had formed the remuneration of the inventor goes to the owner of the machine in which that invention is incorporated? The inventor as such certainly ceases to reap any specific benefit from the time the invention becomes virtually public property. The answer to these questions must furnish the real clue to capital-profit, if it is attributable to the benefit afforded by the use of capital. The hire being now less than the advantage due to the use of the machine, this advantage ceases to determine the hire, and we must look for some other economic factor fixing this rate. Capital will no doubt continue to be invested in the making of sewing-machines as long as the profit resulting from this investment exceeds that which can be obtained from other investments, and the hire will fall as more capital is invested in this branch. Were other forms of capital incapable of returning a profit, the investments in sewing-machines would increase until the profit accruing after deducting risk and deterioration would be only nominal, or practically nil. But other forms of capital being known to bring a revenue, investors will be attracted only so long as the hire of sewing-machines will bring a profit over and above that of other investments. We are thus led to the inference that capital in the form of sewing-machines can persistently bring interest only because other forms of capital are capable of bringing interest. The sewing-machine as such can therefore not account for profit on capital; the cause of interest must be looked for elsewhere, and since the same can be said of all other means of production, we are again compelled to fall back upon the interest-bearing power of money as the cause of all capital-profit, money being the only form of wealth to which an economic cause for interest can be assigned, while laws are in operation which by obstructing commerce render possible the collection of a tell from the toilers.

Doubting that the use of inanimate products can account for the apparent reproductive power of capital, some writers resort to a modification of the utility argument, which may be presented by quoting Jeremy Bentham’s criticism of Aristotle, who held that all money is in its nature barren. “A consideration that did not happen to present itself to that great philosopher, but which, had it happened to present itself, might not have been altogether unworthy of his notice, is, that though a daric would not beget another daric, any more than it would a ram, or a ewe, yet for a daric which a man borrowed he might get a ram and a couple of ewes, and that the ewes, were the ram left with them a certain time, would probably not be barren. That then, at the end of the year, he would find himself master of his three sheep, together with two, if not three, lambs; and that, if he sold his sheep again to pay back his daric, and gave one of the lambs for the use of it in the mean time, he would be two lambs, or at least one lamb, richer than if he had made no such bargain.”

In this illustration we are told of two persons, one having sheep, which have the power of multiplying and are therefore supposed to be capable of spontaneously reproducing value, the other having money, which is acknowleged to be barren; yet one is willing to give his reproductive capital for money which is minus this desirable attribute. To say that with the daric the seller of the sheep might buy other sheep, or wheat, or wine, would be arguing in a circle. Viewing the transaction in the light in which its presentation is intended, it is evident that some one will be deprived of that benefit which the buyer of the sheep can reap; for the darics will continue to exist as darics and are not converted into anything else, and those who unwisely sold their automatic value-producers are just minus the three lambs as a result of their exchanges. There must be some flaw in this argument, for the sellers of sheep are as a rule as shrewd as the buyers. It appears that a consideration did not happen to present itself to the critic of the Greek philosopher, but which, had it happened to present itself, might have deterred him from antagonizing Aristotle. The housing, feeding, and raising of the sheep and lambs require labor, without which the owner of the sheep would not have been the owner of the lambs. Leaving out of account the conditions which give rise to rent, as well as the effects of various restrictions to competition, the value of that labor and the value of the three lambs would be identical. The value of the lambs, then, must be attributed to the labor spent, and not to the reproductive power of the sheep; hence the logic of Bentham falls to the ground.

It is remarkable that this very argument has been revived by Henry George, who has more than any one else contributed towards popularizing the doctrine that the forces of nature cannot produce value independent of the quantity of labor applied, unless the supply is inadequate; and the margin of cultivation being the limit that separates an insufficient from a redundant supply, it manifestly marks the line at which the bounty of nature ceases to have an exchange value. Presuming freedom. of competition, the reproductive powers of nature at the margin can accordingly produce no value beyond that of the labor requisite to aid nature in its processes and to appropriate its gifts.

But even admitting, for the sake of argument, that interest could arise from the creative forces of nature, it remains a mystery as to how this power is imparted to money when loaned. The allegation is that its exchangeability with vital products accomplishes this transfer. This, however, is not a valid reason. Exchanges are consummated on account of the properties possessed by the objects of exchange; but here we are informed that a thing can be invested with a property it does not originally possess by the mere fact of being exchanged for a thing which has that property. This is clearly one of the many instances in which cause and effect are confounded.

Were it true that vital products are capable of bringing interest while money as such is not, then vital products and money would be economically heterogeneous and hence non-interchangeable.

Regarding the abstinence doctrine, its repeated condemnation and revival in modified forms alone is sufficient to betray its weakness. Its modern presentation generally takes the form of the assertion that immediate payments are preferred to premises of future payments. But we cannot be unmindful of the fact that Safe Deposit Companies are even paid for delivering at a future time valuables received at present. This shows that those who accumulate wealth for a future use will prefer a future delivery if it saves the trouble and risk that accompanies the conservation of wealth; provided the factor of risk is absent, and the wealth receivable is not available for profitable investment. The possibility of a profitable investment of capital is therefore one of the conditions under which this argument is applicable, and for this reason abstinence cannot account for interest. In the sense in which it is used by the followers of Senior, abstinence is a voluntary delay of consumption, nothing more; and since no one can deny that the utility of abstinence consists in the ability to consume at a later day that which is not consumed to-day, its natural pay cannot exceed the value of the wealth conserved. The “Element of Time” is frequently mentioned as a factor in the law of distribution, but its exact bearing on the genesis of interest is never made quite clear. If time has any economic effect upon wealth, it is generally one of deterioration, involving a loss of value, the exceptions being rare.

Other arguments are equally doubtful. The assertion that man would not save capital if he could not make it a source of income is an insult to the intelligence of man. While it is true that he will not loan his wealth to any one without interest when he can get interest for the same loan from others, his propensity to accumulate will continue even after all but the natural motives for saving are removed. Man is certainly not inferior to the bee or the badger. That he will provide for the contingencies of the uncertain future even at the risk of loss and deterioration is indisputable.

The expectation to meet, or the fear of, a future want is, however, not the only inducement; there exists another most potent motive for producing capital. Experience has taught that the indirect way of production which brings into requisition auxiliaries of a more or less intricate character is the most fertile and the least irksome method. The accumulation of capital is essential to the saving of labor, and our desire to gratify our wants with the least exertion prompts us to produce these auxiliaries which facilitate production, even if they should lack the power of returning a revenue.

For this reason there is no foundation for the fear that progress will be impeded when capital fails to bring a persistent income. Those producers who employ the most approved method of production will always have an advantage over those who are slow to follow the march of improvement. But even the latter will in time follow in the footsteps of their more enterprising competitors, when a cheapening of the product will transfer the benefit of progress to the consumers, while competition will render retrogression impossible.

Equally groundless are the fears of those who imagine that capital will not be invested and industry will languish when capital ceases to return an interest exceeding its replacement. This pessimism can be traced to a misconception of, and a failure to distinguish between, the functions of the capitalist and of the employer. The fact that they are usually centred in one person is no reason why they should not be separated in an analysis of their relation to production. The capitalist who as such is the owner of the capital and the recipient of interest, is personally inert and is performing no part of the employer’s. and manager’s work, who receives as remuneration for his services what is generally termed business profits, often affected more or less by occasional profits or losses due to speculation or to unavoidable fluctuations of the market, etc. And as the remuneration of labor including the employers’, is increased by a diminution of interest, other things being equal, the inducement to work will really be increased and industry will be encouraged rather than otherwise.

However we view this abstinence doctrine, when brought to its logical conclusion, it fails to show how under free competition in a community capable of producing more than sufficient to satisfy the immediate needs, the difference between the present and future valuation of wealth—which is claimed to determine the rate of interest—can in the average exceed the rate of risk and deterioration, and only in so far as these two elements are more or less proportionate to time, the “Element of Time” can legitimately enter into the discussion in an indirect way.

This concludes the chain of arguments which justify the assertion that involuntary idleness is due to a preventable cause.

The law which denies the producing class the right to issue credit-money, however high their credit may be, operates like the patent laws, which in forbidding to others the use of an improvement justly enables the inventor to reap a part of the advantage which his invention affords; with this difference, that the free use of the invention of credit-money is withheld from the wealth-producers for the benefit of the lenders of money regardless of the time which has elapsed since the invention should have become public property. It makes that usury an economic possibility which Bacon. says “bringeth the treasure of a realm into few hands.” By enabling the owners of money who lend it on interest to acquire a right to demand an annual tribute from others, it gives to money directly, and to capital indirectly, a seeming power of reproduction and endows the dollar with the appropriate attribute “Almighty.” Although Aristotle over two thousand years ago recognized the interest-bearing power of money to be unnatural, yet at the close of the nineteenth century, in which the impossibility of a reproduction of physical energy has been demonstrated, the doctrine that industrial energy in the form of capital is an exception to the otherwise inexorable law of nature still dominates and prevents economic science from rising above the level of the ancient dogmas that physical science has long since discarded. The foremost writers commit themselves to obvious inconsistencies in the vain attempt to give a cogent explanation of the origin of this power. John Stuart Mill, in commenting on the expectations of those who advocate an expansion of credit-money, closes with the remark, “The philosopher’s stone could not be expected to do more,” unmindful of the fact that, under the conditions which he defends, capital, if owned in sufficient quantity, can bring its owner enough of this world’s good to abundantly satisfy the irrational longing of the alchemist. Bishop Berkeley frankly admitted that a bank is a gold-mine, and asks if it is not the real philosopher’s stone; but he failed to see that this magic power can be but the result of political legerdemain.

This same power of money readily accounts for the absence of the equation which naturally should exist between the supply of and the demand for commodities. The medium of exchange being available as a medium of extortion, is desired, not only for obtaining commodities in exchange, but also for imposing tribute. Money being for this reason more desirable than commodities of equal value, the demand for money will necessarily exceed the supply, and reciprocally, the supply of commodities offered for money must exceed the demand. The consequent accumulation of unsold products is often mistaken for the cause of involuntary idleness, while it is but a symptom of commercial stagnation. The amount of work that can be done under the modern system of divided labor is limited, depending upon the amount of products that can be exchanged through the available facilities for exchange, and only a lack of such facilities can account for a scarcity of work in a country so blessed by nature as this. The same fear of a dearth of employment that instigated the silk weavers to destroy the Jacquard loom now prompts legislators to “protect” the workers by’ taxing imports, regulating immigration, passing factory laws, and other similar ineffective enactments. It cannot be denied that while the debtors’ tribute exceeds the risk-premium, an increase of indebtedness by what is called an unfavorable balance of trade will impair the prosperity of a people; nor can it be gainsaid that the immigration of producers, in absorbing a portion of the available medium of exchange and intensifying its comparative stringency, can only aggravate the stagnation of commerce; but these conditions being the effect of an obstruction to exchanges, additional restrictions cannot give relief.

Our investigation has led to revelations which constitute a serious arraignment of our present political institutions. There are laws supposed to protect the toiler in the enjoyment of the fruits of his labor which uphold a system of exploitation under the guise of justice. The accusation is too serious to be met by mere denial or by the recapitulation of untenable doctrines and indefinite statements.

We need look no further to account for the unrest of the producing class who plainly feel an oppression, the exact nature of which they fail to recognize, and who attempt to meet the unfavorable condition by combinations and restrictions wholly opposed to the freedom and independence of intelligent men. While social science defends the power which secures incomes to the possessors of wealth altogether disproportioned to their personal merit, its teachings cannot cope with the plausible arguments of demagogues, nor check the unwise agitation of well-meaning men who advocate everything but the removal of inequitable restrictions as a cure. Nor can it dispel the darkening cloud that overshadows a civilization characterized by an increasing differentiation of rich and poor, by a periodical recurrence of business depressions and a growing discontent of the working classes, manifested in the hostile attitude of labor-organizations. If our financial legislation is really the seat of the disorder, the question of securing remunerative employment to all who are able and willing to work should no longer be considered an unsolvable problem.

APPENDIX.

As regards purely economic research, the study of the monetary flow between the creditor and the debtor class in conjunction with the amount of indebtedness leads to an important discovery. It reveals the law which under present conditions determines the rate of interest proper. Though somewhat abstract, the following deduction of this law may be of interest.

In principle the separation of the financial from the industrial group can be conceived with perfect precision, if it is based upon functional relations and not upon the individuality of persons. In tracing the monetary flow attention must be paid to money rather than to its owners, by classifying the various purposes for which it is used. The financial group being considered the source of all money, each piece passes from it into circulation when used for the first time, and in its further career it may alternately pass from group to group, communication being established by several channels through which it will pass when employed in certain transactions. All money can thus be separated into two distinct volumes, one being dormant in the possession of the financial, the other circulating within the industrial, group.

Regarding the relation of indebtedness, those persons interested in both groups have from the stand-point of our present inquiry a dual existence, their relations to each group constituting them or making them distinct individualities, to differentiate which it is necessary to agree as to what establishes a financial relation. Accepting as financial obligations all interest-bearing debts which by stipulation are payable in money, all persons having such claims are to that extent members of the financial or creditor group, while in every other capacity they with all others are members of the industrial or debtor group.

In deducing the law of interest we must obviously take cognizance of all transactions by which money will pass from one group to the other, as well as those affecting the relation of indebtedness, while all transactions which affect neither the relative indebtedness nor the volume of money in circulation, are of a neutral character and are here of no consequence.

As we have seen, money can be put into circulation only by purchases and by loans, and is restored to the financial class by the payment of the principal of, and interest on, loans. Purchases imply a flow of money from the financial to the industrial group only if the money paid emanates from the financial group, while those made with money already in circulation must be treated as monetary transfers within the industrial group and have no effect upon the flow under examination. All investments in stock, business ventures, etc., should be included in the category of purchases, and the payment of dividends, shares of profits, etc., are neutral transactions. A flow of money in the opposite direction through commerce is precluded, because the selling of goods or services is exclusively a function of the industrial group. The officers of a bank, in selling their services to the bank, are clearly members of the industrial group, they are workmen engaged in directing the flow of money into the most remunerative industrial channels and guarding the security of financial transactions.

Lending money is eminently a function of the financial group, and every flow through the loan channel marks an increase of indebtedness. But when money circulating within the industrial group is used for loans, a difficulty would arise if the recognition of the economic duality of the owner did not enable us to regard the intent to use such money for a loan, as its conveyance from one to the other of the dissociated units of the owner, as a transfer from the industrial to the financial, from which it is returned as a loan to the industrial group.

Sales of commodities on credit, if such debts are interest-bearing, should likewise be considered compound-transactions,—one a complete sale, the other a return of the purchase-money as a loan.

Indebtedness can be terminated either by payment of principal and interest, or by remission, when obligations cannot be met. The risk of losses would not be incurred if the interest paid by the debtors as a whole did not more than cover such losses, so much of the interest as will equal them being the insurance. The monetary flow resulting from the payment of interest is accordingly divided into two branches, the risk-premium, and the interest-proper, the former being equal to the sum total of all relinquished loans.

We now clearly recognize five channels of the monetary flow as represented in Fig. 3. (See plate at end of volume.) By purchases and loans money will flow from the financial to the industrial group, and by Transfers, Cancellations, and Interest in the opposite direction, the interest channel consisting of two branches, Risk-premium and Interest-proper.